How and why to build a CD ladder

Savers looking for a secure way to guarantee the growth of their savings without giving up access to all of it should consider the CD ladder strategy.

Unlike a high yielding savings account, your savings rate is guaranteed with a Certificates of Deposit (CD). But instead of putting a lump sum into one CD, laddering involves diversifying your savings across multiple CDs with staggered term lengths.

How it works

Unlike a single CD where all your funds are locked in for a fixed term, CD laddering allows for more flexibility. It’s called a ladder because each CD has a different maturity date when you can access your funds. Each of these represents a rung in your ladder as you climb from shorter-term CDs to longer-term CDs maturing.

By spreading your savings across these rungs, you gain access to your funds—plus the interest they’ve earned—at regular intervals while still enjoying the benefits of guaranteed interest rates.

As each CD in your ladder reaches maturity, you gain access to some of your savings. You can use those funds to pay for planned expenses or open a new CD and put all or some of the previous CD’s deposit into it.

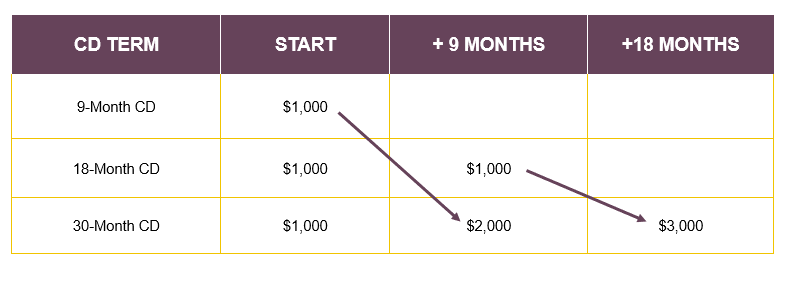

Example: CD ladder with Ardent Flex CDs

Ardent offers Flex CDs with terms of 9 months, 18 months and 30 months. Flex CDs offer the guaranteed interest rates of a traditional CD but have the added benefit of allowing you to withdraw some of your balance prior to maturity without penalty—kind of like a savings account. This provides added flexibility to your CD ladder, as you won’t be penalized if you need funds in between maturity dates.

Imagine you are a saver with $3,000 aiming to help save for a down payment. You could create a three-tiered ladder using one of each Flex CD term:

Sample CD ladder showing principal

As your 9-month CD matures, you can either use that $1,000 principal plus the interest it earned or reinvest it into a new CD as needed.

Pros and Cons of a CD ladder

Pros

- Guaranteed Returns: CDs offer a low-risk, predictable rate of return, providing a shield against potential market fluctuations. The varied interest rates could earn you more over a longer period of time than if you put all your funds into one CD. Plus, CDs from reputable financial institutions are federally insured up to $250,000.

- Enhanced Flexibility: As each CD matures, you have the option to withdraw your funds or reinvest them in a new CD with a longer term.

- Liquidity: Instead of locking away all your savings into one CD where you’ll need to pay a penalty to access it before maturity, a CD ladder maintains a consistent schedule of maturing CD terms. That way, you’ll regularly have access to a portion of your savings.

Cons

- Interest rate changes: You may miss out if rates rise while you have cash locked up in a longer-term CD. You may also miss out on benefits if shorter CD terms pay much higher rates than longer terms. You may not be able to time your ladder to earn you the most.

- Missed opportunities for higher earnings: CDs offer guaranteed returns with low risk, but you may find higher returns with higher-risk investments.

- More effort: CD ladders require more effort and planning since you are opening multiple CDs with terms that align with your future plans, rather than just one account to monitor.

Start building your ladder

While there are plenty of recommendations for CD ladder structures out there, much of it depends on your personal financial circumstances and goals.

- Choose Your Terms: Determine the number of CDs you wish to include in your ladder and the desired maturity dates for each.

- Divide Your Investment: Divide your total savings amount by the number of CDs to determine the initial deposit for each.

- Open Your CDs: Open each CD with the selected term length.

- Reinvest as CDs Mature: As each CD reaches maturity, you can reinvest the principal and earned interest in a new CD with a term that extends beyond your highest rung.

Conclusion

CD laddering is particularly well-suited for savers who prioritize guaranteed returns and a reduced risk profile compared to the stock market, as well as access to funds at regular intervals without compromising earnings. CD ladders may not be right for everyone, but by carefully constructing your CD ladder, you can create a robust and adaptable savings strategy that aligns with your goals.